You Should Be Earning Money

While You Sleep.

Why Your Earnings Are A Fraction of What They Could – & Should – Be.

Investing 101

Every home inspector must build savings – for retirement, for unexpected costs (hospitals, car wrecks, etc.), and for business reserves. That probably is obvious.

What may not be so obvious is how to do that well – and make money on it.

The short answer is that practically all that money should be invested – not left in a bank or CDs. Once it is invested, leave it alone and let it grow.

Basically, retirement and loss reserve funds belong in long-term investments. There are many reasons, including the “miracle of compounding” returns and lower taxes when investments are sold. (There are special tax rules for 401(k) or Roth retirement plans, which are mentioned later. Both have contribution limits). It is true that some ready cash needs to be kept on hand for daily expenses. But most savings, for retirement, for business reserves, and the like, needs to be invested. All retirement and business reserves should be invested long-term. Parked, put to work, and left alone to keep working until retirement time comes.

It is surprising how many home inspectors never get around to taking that important step. Investing lets your money earn money for you, while you work. Banks basically do not.

Let’s say upfront that you do not have to be an investment whiz to do this, and do it well. No one has to watch CNBC all day everyday, or rent a Bloomberg terminal, or read The Wall Street Journal and Barron’s like a religious fanatic to invest successfully. A little of any of those tools works just fine to help think about investing. But it is more important to remember that, by the time anything gets in the media, Wall Street already has made most of the money on the idea. In fact, a little modesty about our skills and knowledge serves us very well in this. No one in Kentucky ever will be able to consistently pick individual stocks better than Wall Street insiders. Trying to do that is a money losing proposition.

Instead, here are the basic keys to get started investing successfully.

First, invest mainly in stocks.

The key point to remember: Stocks as a group (like the S&P 500) have better returns over long periods of time than “safer” types of investments like bonds or money market funds.

Example: If you invested $100 a month for 10 years in the Vanguard 500 Index Fund (which tracks the S&P 500 stock Index), you would have $19,587 as of November. Of that $12,000 would be the money you invested and $7,587 would be gains.

If you invested the same $100 for the same 10 years in the average U.S. government bond fund, you would have $14,607. Of that, $12,000 still would be the money you invested.

Third choice: If you put the same money put in the average money market fund for the same time, you would have $12,589.

In other words, the $12,000 investment is stocks earned $7,587 over the last 10 years, while same investment earned just $2,607 (about one-third as much) if it was in bonds, and only $589 if it was in a money market fund.

That is a very large difference.

The return on investment would be even larger if the whole $12,000 had been put in on the first day, and just left there for all 10 years. Over the last 110 years – which includes the recent financial meltdown – the S&P 500 Index was up 107.4%. The typical S&P 500 Index fund was up 105.3%, after expenses. In other words, those earnings would total $12,888 and your account would be worth $24,888. That’s worth mentioning because you can save at least $17,500 each year in a 401(k) retirement plan. If you are 50 or older, you can save another $5,500, or a total of $23,000.

If something other than an index fund sounds tempting, remember that only 6 of the 25 largest stock mutual funds beat the Vanguard 500 Index fund over the same 10 years. And that was before subtracting loads, costs, and annual fees. So even if fishing in the top 25 mutual funds seemed tempting, the odds of beating an index fund are about 4-to-1 against you. That’s worse than a $20 scratch off lottery ticket, with 3.2-to-1 odds of winning. In other words, the odds of picking one that is a loser compared to the Vanguard 500 Index fund are really, really good. Try flyers, if you must, with a small percentage of your investment.

As a rule of thumb, keep 60% or more of the investments in stock index funds.

Second, beat inflation. Or you will either shrink the money or standstill.

All of those earnings numbers are gross – without adjusting for inflation. It is not enough to see an account balance go up. It must go up more than inflation. Otherwise, there is no “real return” on investment. An account that goes up at exactly the same rate of inflation is standing still in buying power. It is “dead money.” It is not really earning anything. An account that goes up less than the rate of inflation is losing money, by losing real buying power.

“Inflation” measures the purchasing power of money. To have at least as much purchasing power years from now, with any investment, the earnings have to equal or beat inflation. Just think about how much $1 would buy in gas, or milk, 10 years ago, compared to today.

The cumulative rate of inflation since January 2003 is 26.7%. In other words, what you could buy for $12,000 in 2003 would cost $15,200 in November, 2013. (Want to run your own numbers? There’s a handy calculator of actual historical inflation at http://www.usinflationcalculator.com/ and several sites offer projected future inflation calculators, like http://www.bankrate.com/calculators/savings/price-inflation-calculator.aspx?ec_id=m1108602&ef_id=UolikgAABNSSoAXb:20131229181745:s.)

That means a $12,000 investment ten years ago needed to earn 26.7% or more just to break even, and have the same buying power today that it had then. Only stocks achieved that outcome.

Putting money in a bank is losing money at today’s interest rates, and the foreseeable interest rates in the years ahead. The U.S. Federal Reserve says it is targeting holding annual inflation in roughly the 2.5-3.0% range for the next 3-5 years ahead, or more. If your interest rate is 1% on savings or a CD, and inflation is 2.5-3.0%, which is roughly the picture for 2013, then the savings lose 1.5-2.0% a year. The number in the account balance does not go down. What you can buy with the money goes down. It’s like a hidden bank tax. To make matters worse, banks are constantly sucking off money in fees and charges. Savings in banks is getting as overloaded with hidden charges as flying airplanes.

Third, minimize costs and expenses. There are no good “free” investments out there. But there are plenty of ways to invest that are thousands, even tens of thousands, of dollars more expensive every year.

There are two basic ways to cut costs and expenses to the bare minimum.

Begin by picking low costs investment strategies, such as a “passive” stock index fund. There are no lower entry costs and no lower annual fees in investing.

Low cost investment strategies also mean using only low cost investment advice.

When it comes to sales charges, fees, and costs, the sky is the limit. Generally, the government imposes no limit on mutual fund or investment advisor fees. There are sales “load” fees, management fees, account fees, redemption fees, exchange fees, distribution and service (12b-1) fees, and even, after all that, “other fees.” (There’s more at http://www.sec.gov/answers/mffees.htm.) Every fee and cost charged keeps nibbling at the return on any investment perpetually. The more nibbles, the more the investment gets eaten up. That is something is it vital to avoid.

Let’s say your mutual fund returned 10% in a given year. If you had paid a load of 3%, 12b-1 fees of 0.5%, and a management fee of 1%, then your 10% gross return would yield only 5.5% to you, meaning you’ve lost almost half of the returns to fees. Even a no-load fund (or a front-loaded fund in year two) would still see you paying 15% of your profits to a fund manager who most likely underperformed the market anyway. The now-classic book, Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor by John Bogle, founder of the Vanguard Group, is a “must read” to learn more.

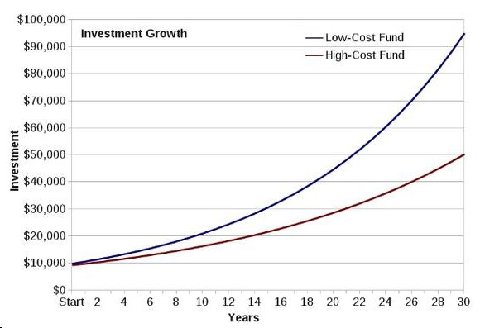

Let’s look at an example to do the numbers. Imagine two investors, each investing $10,000 in funds that grow 8% per year over a 30-year time frame.

The low-cost investor pays 0.2% per year, meaning her net return per annum is 7.8%. Over 30 years, this results in a balance of $95,184.

The high-cost investor pays an initial 5.75% in front-loaded fees, management expenses of 2% per annum, and 0.25% 12b-1 fees. So, right off the bat, the initial investment amounts to $9,425, not $10,000, due to the front-load fee. Then, each year for 30 years, the net return is 5.75% due to the annual fees. The balance at the end of 30 years? About $50,000.

That’s a big difference. Like double your money – or cut it in half with fees and cost.

Source: Bogleheads.org; see also http://www.fool.com/investing/general/2013/12/23/why-active-mutual-funds-destroy-value.aspx#.UsB8PpvW46w

Here are some details:

The first step is to use “passive” investments, like an “index fund.” Over the years, that always beats similar investments that have “loads” (sales commissions) and where there are fees and costs, for example in a mutual fund or “active” investment management.

Our basic suggestion is to use a low cost S&P 500 index fund, such as Vanguard’s, for the major investment, as long-term readers of PLI’s Newsletter know.

“Index funds” are “passive” investments in bundles of assets, like stocks. Vanguard basically invented index funds, and still delivers them more cheaply than practically all other forms of investment. “Index funds” hold a collection of stocks, such as the 500 big company stocks tracked by Standard & Poor’s, known as the S&P 500. Other broad index funds will do too, such as Vanguard’s total stock market fund (VTI). But narrower “sector” funds, like technology stocks, or retailers, are more of a gamble and should be much smaller parts of a retirement fund’s overall investment.

Index funds do not have managers actively picking stocks. They just duplicate the basket of stocks in an index, like the S&P 500, so it’s brain dead. There is no stock picking to do. That means costs and annual fees are in the bargain basement. The lower the costs and fees, the more an investor keeps.

Over the long term, “passive” investments – like index funds – outperform “active” managed mutual funds and stock picking, mainly because of the extra costs of active managers and stock pickers. Inspectors interested in the arithmetic can find a quick summary at http://seekingalpha.com/article/1917651-have-index-funds-become-too-popular?source=email_mac_mar_out_4_5&ifp=0). And the longer the investment, in time, to more “active” investors are going lose. 1991 William Sharpe wrote a paper “The Arithmetic of Active Management.” http://www.stanford.edu/~wfsharpe/art/active/active.htm; See also The Five Myths of Active Management by Berk, an excellent paper. http://faculty.chicagobooth.edu/john.cochrane/teaching/35150_advanced_investments/Berk_myth.pdf.

Source: (no copyright) http://en.wikipedia.org/wiki/File:Great_Seal_of_the_United_States_(obverse).svg

.svg){kind=link}

Next, minimize the tax bite. That means using tax-free retirement funds for as much of the investment as possible. For most home inspectors, the main tools here are 401(k) plans and Roth plans. In a 401(k) you get a tax deduction for all contributions and earnings in the account accumulate tax free. The trade-off is that all distributions are taxed – but normally at a lower, post-retirement rate. That’s a good deal. Every home inspector should take advantage of it. In a Roth plan, the money contribution is taxed, instead of being deductible. But it still earns and compounds tax free. Better yet, money taken out in distributions from your Roth plan also is tax free. That’s a great deal. Not taking advantage of it would be a mistake.

Outside of those tax “qualified” retirement investments, cutting down taxes means always holding investments at least one full year before selling. That cuts the “capital gains” tax roughly in half. The tax on earnings from capital assets, like stock, sold after one year typically is 20% or less, lower than the tax on ordinary income, which can be 39.6%. Gains on stock sold in less than one year are taxed at the seller’s ordinary income tax rate. In other words, selling short term – in less than a year after buying a stock – can almost double the taxes taken out. (“Capital gains” are the dollar difference between the cost “basis” of an asset, like stock, including brokerage costs, and the sale price. That profit is a “capital gain.” A loss is a “capital loss.” The percentage of tax, especially for dividend income from stocks, depends on the individual tax bracket.)

Fourth. Increase the amount you sock away. Max it out if you can.

That 401(k) can invest an additional $17,500, complete with a tax deduction on this year’s return. Add another $5,500 if you are 50 or older – for a total $23,000 tax deductible investment in your future.

In addition to your 401(k) contribution, inspectors also can stockpile another $5,500 in a Roth or IRA plan. For inspectors over 50, you can add $1,000 more, for a total retirement plan deposit of $6.500.

The same limits apply for 2014 contributions.

It’s not too late. As usual, contributions for 2013 can be made as late as April, 2014 for your 2013 federal tax return.

PLI thanks its financial advisor, Darrell Thomas of Wells Fargo Financial Advisors, for review and comments on this article. The opinions expressed are solely those of the author.